When Good Intentions Lead to Bad Outcomes

The Valuation Shortcut

Some property owners skip professional valuations, instead estimating replacement costs themselves or simply increasing last year's sum insured by inflation rates. This approach inevitably leads to underinsurance. Construction costs don't follow standard inflation, they fluctuate based on material costs, labour rates, and building standards.

Professional valuers account for all rebuilding costs: demolition, debris removal, professional fees, building permits, and compliance with current codes. DIY estimates miss these components, creating cover gaps that surface during claims. A R3,000 valuation fee seems expensive until a R100,000 claim shortfall materialises.

The Cover Reduction Gamble

Reducing cover limits or increasing deductibles to lower premiums creates false economy. You shift risk from the insurer to yourself, acceptable if you have reserves to cover potential losses, dangerous if you don't. Many people reduce cover without understanding the financial exposure they're accepting.

Your broker analyses your financial position and risk tolerance before recommending cover adjustments. They distinguish between smart cost management and dangerous exposure. If budget constraints require premium reductions, they'll identify the least risky ways to achieve savings.

The Cost of Being Wise

Adequate insurance costs more than inadequate insurance, initially. Over time, proper cover proves far less expensive than claim shortfalls, out-of-pocket losses, and financial stress. Insurance exists to transfer risk you cannot afford to self-insure. Undermining that transfer defeats the purpose.

Professional brokers provide value beyond policy placement. They prevent costly mistakes, identify cover gaps, negotiate competitive rates, and advocate during claims. Their expertise costs you nothing, commission comes from insurers, yet protects you from expensive errors.

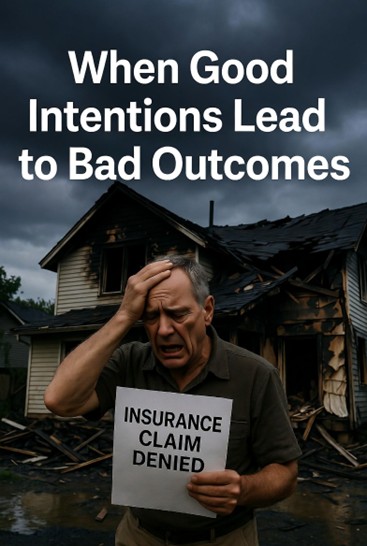

The Averaging Trap

Underinsurance triggers averaging clauses that reduce all claims proportionally. Insure for 70% of replacement value, and you receive only 70% of every claim, regardless of size. A R300,000 claim pays R210,000. You fund the R90,000 difference from savings, loans, or credit.

This mathematical certainty makes underinsurance indefensible. The premium savings from reduced cover rarely justify the claim penalties. Your broker calculates the true cost-benefit of cover adjustments, ensuring any changes make financial sense rather than creating hidden exposure.

Invest in proper insurance advice. Your broker's expertise prevents expensive mistakes, ensures adequate cover, and provides peace of mind. The conversation costs nothing, but the protection it provides is priceless. Contact your broker today for a comprehensive cover review, before you need to make a claim.